Ideas are a dime a dozen. Everyone has them.

Some ideas are great, and others could be improved.

As an online marketer, I've heard countless business pitches from prospective entrepreneurs over the years. While I admire their creativity, just coming up with an idea alone is far from having a viable business concept.

If you are ready to put your idea to the test and launch a startup company, I encourage you to read this guide.

Your idea needs validation.

The last thing you want to do is launch a new business and realize six months down the road that it wasn't a good idea. By this point, you've already sunk too much time and money into the venture.

Don't skip any steps in the startup process.

Here's what I've done. I've outlined how you can take an idea and turn it into an actual business. I've tried to keep this guide as general as possible so that it can speak to the widest audience of entrepreneurs.

For example, some businesses will need to buy or lease retail space. Other brands will need production equipment or partnerships with manufacturing facilities.

Some of you may even need permits and have to meet certain legal obligations before your launch. I stayed away from going into depth on these types of details.

That said, this is an excellent reference for anyone with a business idea and no experience launching a startup.

Even if you've been part of startup launches before, this guide can help you avoid some mistakes you may have made in the past.

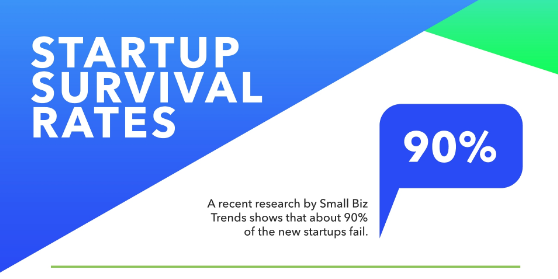

When you approach your new business venture without a plan, you increase your chances of failure.

The odds are already working against you since such a large percentage of new startup companies fail.

You need to do everything possible to try to give yourself an advantage and increase your chances of success.

Here's a pretty common conversation I have with entrepreneurs. They pitch me an idea and follow up with something like, "Wouldn't that be a great business?"

My honest answer is I truly don't know. And they don't know either.

Many ideas sound good when they're verbalized. But when it comes to the logistics, finances, and other important details, the idea may not be as good as you initially thought.

That's why you need to learn how to write a business plan for your startup company.

Your business plan will help you tremendously and ultimately increase your chances of succeeding.

Startups with a business plan have a 29% greater chance of securing funding, which we'll discuss in greater detail shortly. Writing a plan also increases the chances of business growth by 50%.

These are the common components of a business plan:

Your plan will outline everything you need to do, even if your idea is very simple. For example, let's say you're planning to sell shirts.

How are you going to sell them? Where will you sell them? Whom will you sell them to? At what price will they be sold?

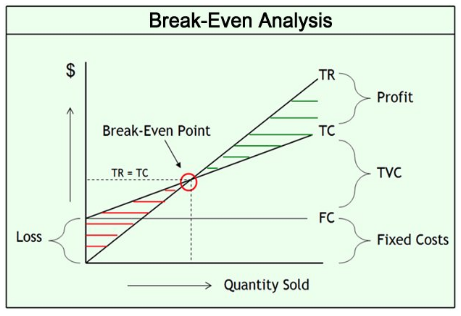

You'll explain in detail your costs to produce the shirts. The business plan will even outline when you plan to break even on your investment.

The financial projections section is arguably the most important part of the entire plan.

You need to come up with realistic numbers. In addition to listing all your expenses, you need to project your sales.

This information will help you determine if your new business can generate money. You'll be able to come up with price points so you can turn a profit.

Again, you must figure all this out before you open the doors of a new business. It starts with proper planning.

The idea for your new business might sound good, but for whom is it a good idea?

Whether you have a product, service, invention, or modification to an existing product, you need to clearly define whom you're selling to.

I hear people say all the time:

"Everyone will like this idea."

This is simply not true. Plus, from a marketing perspective, it's unreasonable to try to launch a brand intended for everyone.

Imagine trying to come up with promotions that appeal to men, women, and children of all ages from every corner of the world. It's not a realistic approach.

You need to learn how to identify the target market of your startup.

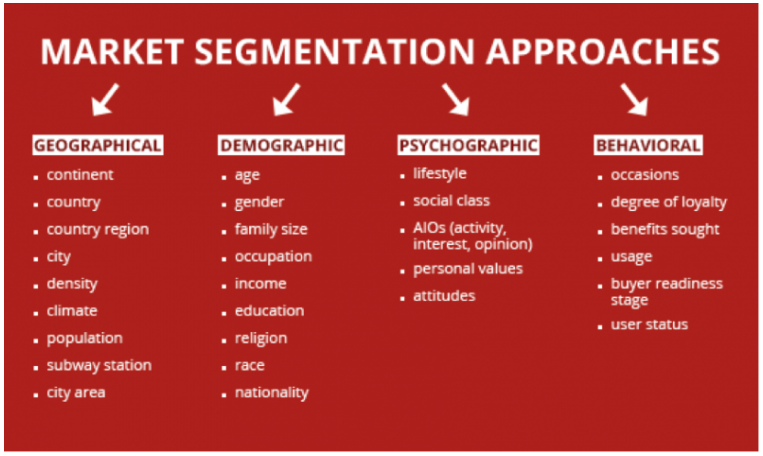

Start with broad assumptions about your prospective customers, and narrow it down even more.

Begin with factors such as their ages, genders, and physical locations. Then get more specific, and identify their interests and lifestyle habits.

Here are some ways for you to segment your audience based on geographic, demographic, psychographic, and behavioral categories.

For example, let's say your product is intended for males between the ages of 25 and 40. That's still a broad audience.

You can make it more specific by saying you're targeting males between the ages of 25 and 40, who live in the United States, make more than $60,000 per year, and are interested in fitness.

Do you see the difference? That's much more detailed. You can develop a customer persona to help you with this process.

Also, you need to look at your target audience from different perspectives. Let's say you're launching a startup that sells toys for young children.

That's not necessarily your target market.

Three-year-old kids don't buy stuff. You need to target their parents instead. Make sense?

Now that you have an idea of whom you want to target, it's time to test that theory. Just because you think your idea is great for a specific market doesn't mean this is true. You can use:

You need to get out there and talk to people. Validate your idea.

It's also necessary to figure out who else is offering the same thing you are. Today, it isn't easy to come up with an idea that's 100% unique.

Don't get me wrong: it doesn't mean you can't make money by having the same idea as someone else. But if the market is oversaturated, it might not be in your best interest to proceed.

I'll give you a simple example to explain what I mean. Let's say you want to open a pizza shop in your city.

You've scouted out a location that can fit your ovens and tables. You can rent it at a reasonable rate. Your pizza recipe is outstanding. Plus, everyone likes pizza, and more than 100,000 people live in the city.

This idea must be a homerun, right? Not if there are 20 other pizza shops within a few blocks of your prospective location.

It's going to be too difficult for you to compete with a market that's so saturated.

This is an example on a small level, but you can scale it to any industry. Look at the ecommerce space. There is a huge competition globally.

In addition to niche brands, you'll also be competing with giants such as Walmart and Amazon.

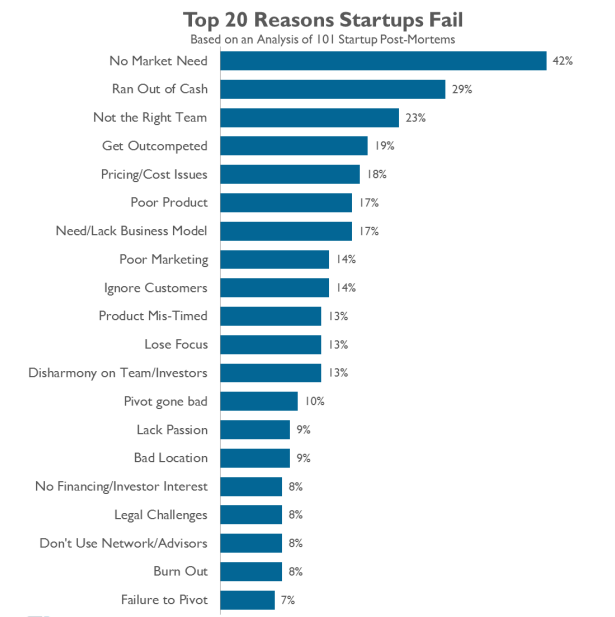

The number one reason why startups fail is that there is no market need.

While your idea might be cool, there may not be a need for your product or service.

Or even if the market needs what you're offering, it could be getting it from someone else already.

Market research will also require you to analyze your competition.

Your startup company needs to have a differentiation strategy that separates you from your competitors.

What's your identity?

Your brand may be cool, edgy, and trendy. Or maybe you're going for a brand identity that is conservative and family-oriented instead.

Some startups launch with a mission to help a greater cause, such as a nonprofit organization.

No matter what your brand identity is, it needs to be clear to your audience. All of your branding campaigns will reflect the image you're trying to portray.

Your website colors, marketing campaigns, and promotions will speak to your brand identity. This even relates to your logo and the name of your startup.

Come up with a name that doesn't restrict your growth. Even if you're focusing on something specific right now, you don't want the name of your brand to put you in a box, preventing your expansion in the future.

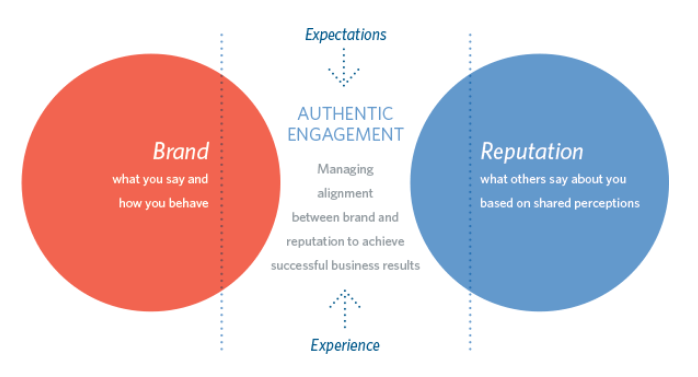

Your brand needs to speak to your target audience, which was already defined. A proper branding strategy will nurture your brand reputation.

In a perfect world, your brand image and brand reputation will be the same. You want people to see your company in a positive light.

So it's important to get your branding strategy right the first time because your reputation is going to stick with you for years to come.

It'll be hard to rebrand yourself in the future if you make a mistake during the launch stages, so don't rush into anything.

It's time to assemble your team.

The size of your team will vary based on the type of business you're launching.

You want to find people strong in areas where you are weak. For example, if you're extremely creative but don't have managerial skills, it doesn't make sense to bring another creative mind on board without hiring someone who can manage employees.

Or let's say you're building a mobile app but don't have any experience with coding or design. You'll need to hire a developer and designer.

Surround yourself with people whom you are compatible with. You want to build strong working relationships with your team.

Here's another problem I see all the time. People launch a startup and just start hiring their friends and family.

Don't get me wrong — this can work. But you need to think long and hard about this decision. Do you want your personal relationships to be impacted by the business?

Can these people take directions from you? What if you need to fire your best friend?

These are all sticky situations, so tread carefully. You also need to make sure every member of your team can bring something to the table.

Just because you were bouncing ideas off a friend a few months ago doesn't mean they're part of the business.

I'm not saying you need to be selfish or stingy, but ultimately, you need to do what's best for you and your business.

Your startup will need some money to get off the ground. Depending on what you're doing, this can range anywhere from a few thousand dollars to millions of dollars.

Everyone's situation is different. You'll need to recognize all your business costs. Here are some examples to consider:

You need to realize you won't have any income when you first launch, but you'll still need to cover all your expenses.

Based on this information, you'll be able to determine how much money you need. Learn how to get your startup funded.

Use your business plan and financial projections when you're speaking with prospective lenders or investors.

You may consider getting a bank loan and pay interest fees for the funds you borrow. But big banks may not be your best bet. Just look at these approval rates for small business loans:

For your startup company, you may want to consider some alternative options:

These are all reasonable sources to raise capital to launch your startup. You'll just have to consider these options and decide which ones are the best for your scenario.

Figure out if it's worth giving up equity in your company. Will your investors bring anything else to the table besides cash?

While it may be nice to have other opinions, you want to make sure you have the final say in all decisions. There is nothing wrong with giving up some equity, but just don't lose control of your company.

Everything is falling into place.

Your business plan looks good. The target market is clearly defined. All your market research is complete.

The team you assembled is qualified. All of your funds have been secured.

Now it's time to put your company branding strategy to work.

Buy a domain name. Launch your website. Create social media profiles.

Start to market your brand. Even if you're not officially launched or selling anything just yet, you can still take pre-orders.

Create a blog. Try to get featured on press releases or news articles. Send free samples to influencers.

Do anything that will make your presence known. Get creative with guerilla marketing and content marketing strategies.

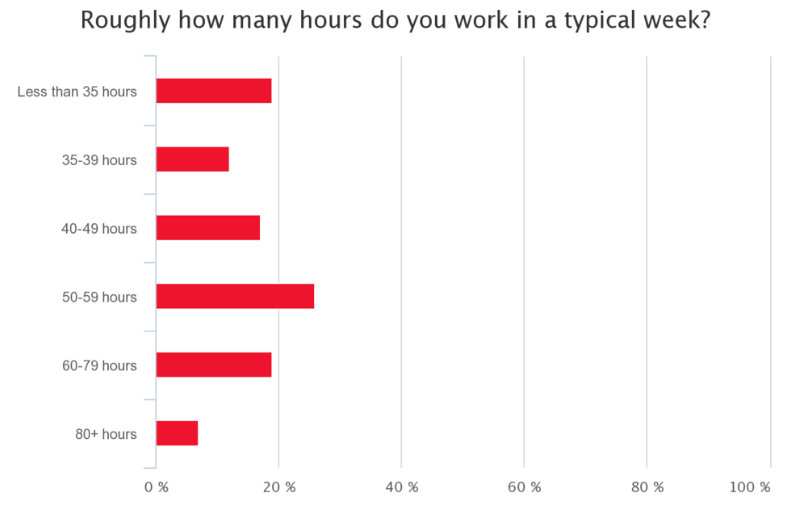

Before you officially launch, you need to ask yourself if you're ready to work.

Sure, you know your idea is great and it's been validated through your research. But are you ready to take the plunge into entrepreneurship?

Just look at how many hours the average entrepreneur works per week:

In order to launch your startup, you might be leaving a job with a steady paycheck to work twice as hard on your new business, without being able to pay yourself for years.

Is this something you can handle mentally and financially?

Research shows 41% of entrepreneurs say they feel stressed almost every day. An additional 33% say they feel stressed a couple of times per week.

But only 7% of entrepreneurs say they never feel stressed.

Unlike with a regular job, there's no quitting on your own business. You can't call in sick when you don't feel like working.

You're the boss. You set the tone for the entire culture of the company.

While being your own boss definitely has lots of benefits, it also comes with added responsibility and plenty of sleepless nights. You need to recognize that your startup can still fail.

I'm not saying all of this to discourage you from following through with your plan, but you need to accept this reality.

But if you're willing to take these risks and get to work, proceed with your business plan, and make it happen.

There is a big difference between an idea and an established business. You need to take steps to validate that idea before you launch a startup company.

Write a business plan. Identify your target market. Conduct market research.

Then you'll need to come up with a branding strategy.

Assemble your team. Surround yourself with people who can contribute to the success of your new business.

Recognize your costs and outline your financial projections. This will give you a better idea of how much money you need to launch your company.

Being an entrepreneur can be rewarding, but it's no walk in the park. You need to ask yourself if you're capable of being a business owner.